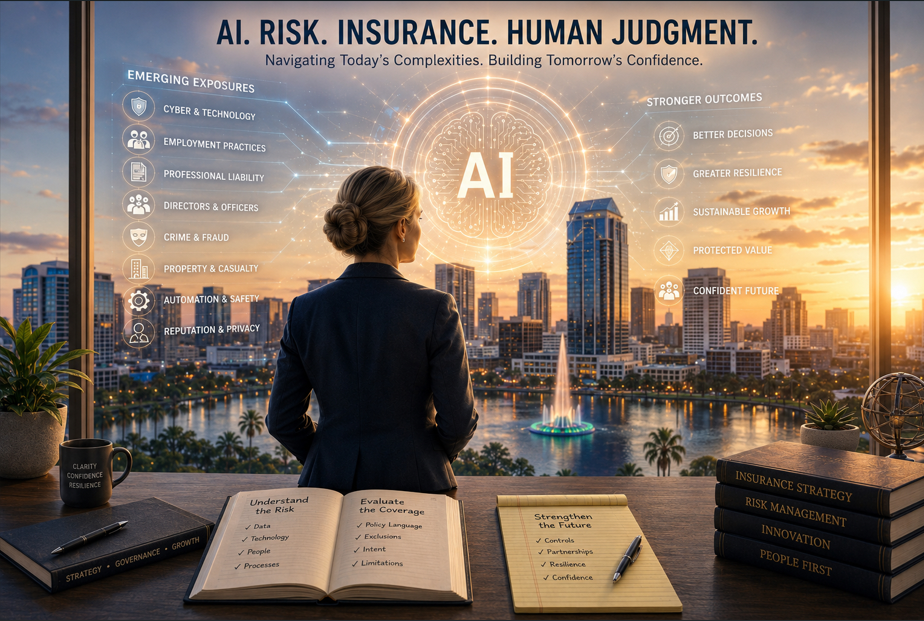

Artificial Intelligence and the Next Great Insurance Coverage Questions

Why PEOs, Risk Managers, and Private Equity Investors Should Be Thinking Beyond Cyber Liability

Reni Snider, Senior Account Executive, Libertate Insurance

Artificial intelligence has rapidly moved from a future concept to an operational reality.

Across the PEO industry, AI is already being deployed to support nearly every facit of life.

Recruiting, employee onboarding, benefits administration, customer service, claims management, compliance monitoring, payroll operations, workforce analytics, sales enablement, and countless other functions.

Most discussions surrounding AI risk have focused on cyber liability.

That focus is understandable, but it is also incomplete.

Cyber insurance may ultimately become only one component of a much broader insurance conversation.

What happens when artificial intelligence begins participating in decisions that were historically made by humans?

The answer affects nearly every line of commercial insurance.

Just as the insurance industry spent two decades grappling with “silent cyber” exposure—cyber-related losses arising from policies that were never designed to contemplate cyber events—we may now be entering an era of “silent AI.”

Across many policy forms, artificial intelligence is being actively used by insureds while coverage language remains largely unchanged.

For PEO operators, risk managers, and private equity investors, understanding where these emerging exposures exist may become a critical component of enterprise risk management over the next several years.

The Cyber Liability Discussion Is Only the Beginning

Cyber liability remains the most visible AI-related insurance issue.

The rise of generative AI has dramatically increased the sophistication of phishing attacks, social engineering schemes, and business email compromise events.

Deepfake technology now allows criminals to replicate voices, images, and even live video interactions with alarming accuracy.

A fraudulent voicemail from a CEO instructing a finance employee to transfer funds once seemed implausible.

Today, it is a realistic threat.

Similarly, employees are increasingly utilizing public AI platforms in ways that may unintentionally expose confidential information, proprietary intellectual property, customer records, or sensitive employee data.

Many cyber insurers have already begun addressing these issues through AI-specific endorsements, deepfake coverage provisions, affirmative AI language, or exclusions.

One reason cyber insurers have moved more quickly than other lines is that cyber policies are relatively modern products with established mechanisms for responding to rapidly evolving technology risks. By contrast, many traditional commercial policy forms are built on decades-old language and loss experience, making insurers hesitant to introduce AI-specific wording before claims trends and legal standards become clearer.

However, cyber liability represents only one piece of the overall risk landscape.

The more significant development may be the expansion of AI into operational decision-making.

Employment Practices Liability: Where AI and Human Resources Collide

For PEOs, one of the most immediate areas of concern is Employment Practices Liability (EPLI).

AI-driven recruiting platforms are becoming increasingly common.

These tools can review resumes, rank applicants, identify preferred candidates, recommend compensation levels, and even assist with promotion or termination decisions.

The efficiency gains are substantial.

The risk, however, is that employers remain responsible for the outcomes.

If an AI model disproportionately excludes applicants based on age, gender, disability status, race, or another protected characteristic, the employer—not the software provider—may ultimately become the target of litigation.

Even when no intentional discrimination exists, disparate impact claims can arise.

The challenge for employers is straightforward:

The use of AI does not eliminate responsibility for employment decisions.

It simply changes how those decisions are made.

Organizations adopting AI-assisted hiring, promotion, compensation, and workforce management systems should ensure that appropriate governance, oversight, documentation, and human review remain part of the process.

Notably, most EPLI policies have not yet been revised to specifically address AI-assisted employment decisions. Insurers face a difficult challenge: employment laws governing AI are still developing at the federal, state, and local levels, and carriers generally prefer not to rewrite policy language until they better understand how courts and regulators will allocate responsibility among employers, software vendors, and individual decision-makers.

Professional Liability and Errors & Omissions: The Human Judgment Question

Many observers believe professional liability and Errors & Omissions coverage may ultimately experience some of the most significant AI-related exposure growth.

Across professional service industries, AI tools are increasingly assisting with analysis, recommendations, forecasting, and decision support.

Accountants use AI to evaluate tax scenarios.

Consultants use AI to create strategic recommendations.

Engineers use AI-assisted design tools.

Attorneys utilize AI for research and drafting.

The underlying legal question is likely to remain the same:

Did the professional exercise independent judgment?

If a client suffers financial harm and alleges that a professional simply accepted an AI-generated recommendation without sufficient review, litigation may follow.

Conversely, situations may arise where a professional ignores a valid AI recommendation and is later accused of failing to utilize available technology.

In many cases, AI does not remove professional responsibility.

Instead, it may create additional expectations regarding how professional judgment should be exercised.

Insurers have been slow to introduce AI-specific E&O endorsements in part because professional liability policies are already designed to respond to evolving standards of care. Until courts establish whether AI use changes those standards—and if so, how—many carriers appear content to rely on existing policy language rather than risk creating unintended coverage expansions or restrictions.

Directors & Officers Liability: The Governance Challenge

Boardrooms are beginning to face a new category of responsibility.

Historically, boards have been expected to oversee financial controls, cybersecurity, regulatory compliance, and enterprise risk management.

Increasingly, AI governance is joining that list.

Investors, regulators, and stakeholders are beginning to ask questions such as:

How is AI being utilized within the organization?

What controls govern its use?

How is data being protected?

What decisions are being delegated to AI systems?

What processes exist to validate outputs?

For publicly traded companies, AI-related disclosures may become an area of increasing scrutiny.

For private companies, private equity investors and lenders may begin evaluating AI governance as part of broader operational diligence.

The issue is not necessarily whether AI is being used.

The issue is whether leadership understands how it is being used and what risks accompany that use.

Many D&O insurers are monitoring these developments closely, but broad policy form revisions have been limited. A primary reason is that AI governance claims have not yet generated a sufficiently mature body of litigation to establish predictable loss patterns, making it difficult for insurers to draft targeted language with confidence.

Crime Coverage and Financial Fraud: A Rapidly Evolving Threat

Crime coverage may represent one of the fastest-moving areas of AI exposure.

Traditional fraud schemes relied upon deception.

AI dramatically improves the effectiveness of that deception.

Voice cloning, video impersonation, synthetic identities, and highly personalized phishing attacks are becoming increasingly difficult to identify.

Organizations that once relied upon verbal confirmation procedures may discover that verbal confirmation is no longer sufficient.

This creates an important coverage question.

Many crime policies were drafted long before deepfake technology became commercially accessible.

As claims emerge, insurers and policyholders will increasingly examine whether existing policy language adequately contemplates these new forms of fraud.

For PEOs handling payroll, benefits administration, employee records, and financial transactions, this exposure deserves particular attention.

Although some insurers are exploring endorsements addressing deepfakes and AI-enabled impersonation, many remain cautious because fraud schemes evolve faster than policy drafting cycles. Carriers are also waiting to see how courts interpret existing fraud, forgery, and social engineering provisions before committing to broader form changes.

Workers’ Compensation and Workplace Risk

At first glance, AI appears likely to reduce workers’ compensation losses.

In many cases, it probably will.

Predictive analytics, safety monitoring systems, ergonomic assessments, and operational automation all have the potential to improve workplace safety.

However, new exposures may emerge as well.

Organizations are already experimenting with AI-driven productivity monitoring, workforce analytics, and performance management systems.

These technologies can increase efficiency, but they may also contribute to cognitive overload, distraction, fatigue, and other workplace stressors.

In manufacturing, logistics, transportation, and warehousing environments, human-machine interaction will become increasingly important.

As intelligent systems begin participating in operational workflows, risk managers will need to understand how those interactions affect injury frequency, injury severity, and overall loss trends.

This is particularly relevant as workforce demographics continue to evolve and employers seek ways to support an aging workforce through technological augmentation.

Workers’ compensation insurers have generally not introduced AI-specific policy language because workers’ compensation systems are heavily statutory in nature. Coverage obligations are often dictated by law rather than policy wording, reducing the need for immediate form revisions even as insurers study how AI may affect workplace injury patterns.

Product Liability and Technology Liability: The Next Frontier

Perhaps the most significant long-term exposure involves products and services that incorporate AI directly into their operation.

Historically, product liability claims focused on manufacturing defects, design defects, and failure-to-warn allegations.

AI introduces an entirely new category of questions.

What happens when an AI-enabled product makes a decision that contributes to an injury?

Who bears responsibility?

The manufacturer?

The software developer?

The business deploying the technology?

The end user?

These questions are already emerging in sectors such as healthcare, transportation, robotics, industrial automation, and consumer technology.

The legal framework surrounding these issues remains largely unsettled.

As a result, insurers, reinsurers, attorneys, and regulators are all closely monitoring developments.

The absence of clear legal standards is one of the primary reasons insurers have not yet broadly revised product liability forms. Until courts establish how liability will be allocated among multiple participants in the AI ecosystem, insurers face significant uncertainty in attempting to draft precise coverage grants, exclusions, or endorsements.

The Emerging “Silent AI” Problem

The insurance industry’s experience with cyber provides a useful historical comparison.

For years, cyber losses were covered—or disputed—under policies that had never been designed to address cyber exposures.

The result was widespread uncertainty regarding coverage intent.

Eventually, insurers responded by introducing cyber exclusions, affirmative cyber coverage grants, dedicated cyber policies, and specialized endorsements.

Artificial intelligence may be following a similar path.

Today, many organizations use AI throughout their operations.

At the same time, many insurance policies contain little or no explicit AI language.

That does not necessarily mean coverage exists.

It does not necessarily mean coverage is excluded.

It often means the answer remains unclear.

One reason this ambiguity persists is that insurers are still confronting fundamental questions about how AI should be defined. Policy language must be precise, yet AI encompasses everything from simple algorithms and predictive analytics to autonomous decision-making systems and generative models. Drafting language that captures the intended exposure without creating unintended consequences is far more difficult than it may initially appear.

For risk managers, ambiguity is rarely a desirable outcome.

What PEO Operators and Investors Should Be Doing Today

The objective is not to avoid AI.

The productivity benefits are simply too significant.

Instead, organizations should focus on understanding where AI is being utilized and how existing insurance programs respond if something goes wrong.

Several practical questions can help guide that evaluation:

Which AI platforms are currently being used?

Are employees permitted to use public AI tools?

What information can be uploaded into those systems?

Which business decisions involve AI-generated recommendations?

What governance controls exist?

How are outputs reviewed and validated?

Do key insurance policies contain AI-specific language, exclusions, or endorsements?

Are vendors contractually assuming responsibility for AI-related failures?

For private equity investors, these questions may soon become a standard component of operational diligence.

For PEO operators, they may become a critical component of enterprise risk management.

For insurance professionals, they represent one of the most important emerging coverage discussions in the marketplace.

Given the current lack of standardized AI endorsements across most commercial lines, organizations should not assume that silence in a policy equates to certainty. In many cases, insurers themselves are still evaluating how AI-related claims will fit within existing coverage frameworks.

Final Thoughts

Artificial intelligence is not simply another technology trend.

It represents a fundamental shift in how information is created, analyzed, communicated, and acted upon.

As AI becomes increasingly embedded within business operations, insurance coverage will inevitably evolve alongside it.

The organizations that benefit most from AI over the coming decade will likely be those that approach adoption thoughtfully—embracing the operational advantages while maintaining appropriate governance, oversight, and risk management discipline.

The key question is no longer whether AI will affect commercial insurance.

The key question is how quickly policy forms, underwriting practices, and risk management strategies will adapt to a world where humans are no longer the only participants in the decision-making process.