Workers’ Compensation Is Becoming More Predictive

Reni Snider, Senior Account Executive, Libertate Insurance

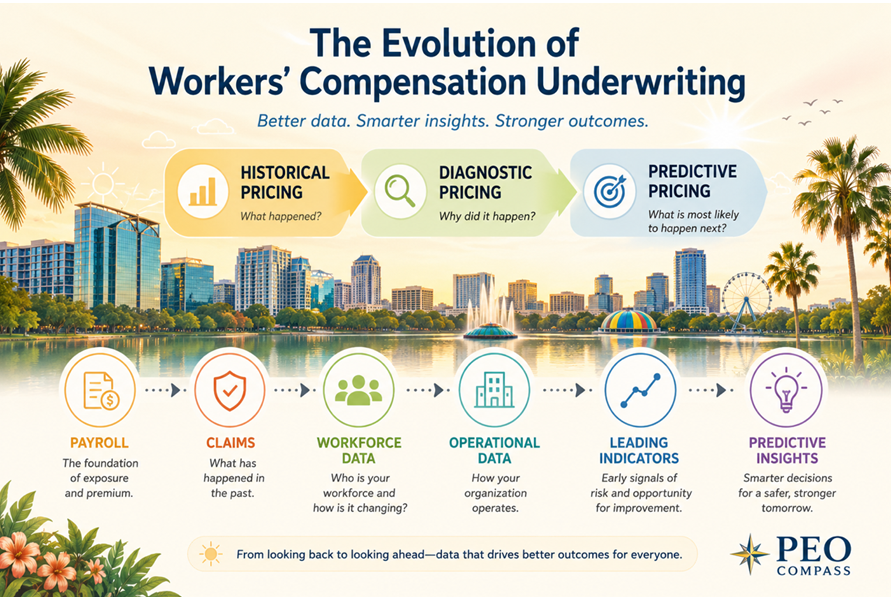

For decades, workers’ compensation underwriting has largely been an exercise in looking backward.

Underwriters examine reported payrolls, class codes, experience modifications, prior losses, and historical trends to estimate future outcomes. Those measures remain foundational to the workers’ compensation system and continue to provide valuable insight into organizational risk.

However, the industry is increasingly asking additional questions.

Rather than simply asking, “What happened?” underwriters are increasingly attempting to understand, “What is most likely to happen next?”

The advent of newly emerging predictive modeling tools is driving one of the most important developments in modern workers’ compensation underwriting. The industry is moving from a predominantly historical pricing model toward one that is increasingly forward looking, supported by growing volumes of increasingly granular data.

For Professional Employer Organizations (PEOs), this evolution presents both opportunities and challenges.

Organizations that understand what these data points actually mean and how they influence future performance will likely be better positioned to differentiate themselves in an increasingly data-driven marketplace.

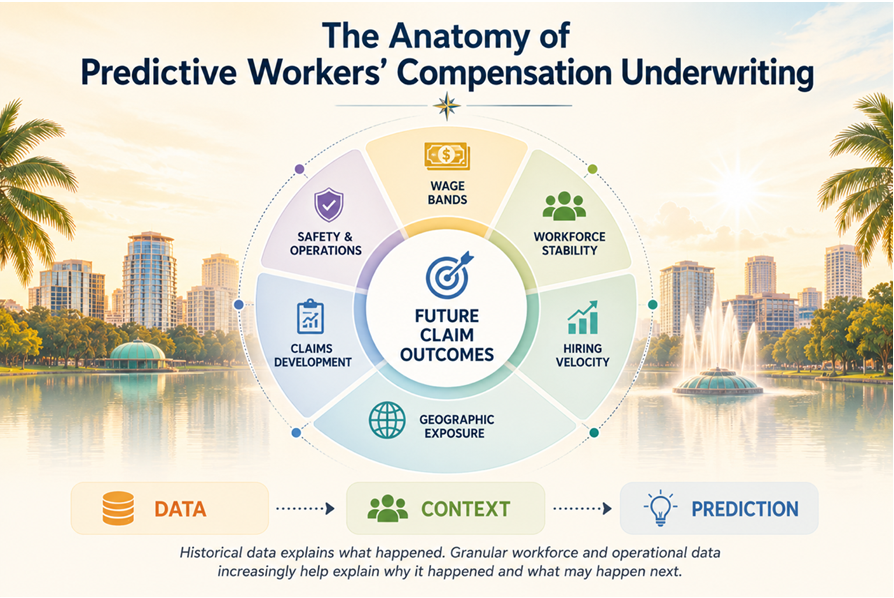

More Data Does Not Necessarily Mean Better Decisions

The workers’ compensation industry has never suffered from a lack of information. Carriers, TPAs, brokers, and PEOs have long possessed enormous quantities of claims, payroll, and policy data.

The difference today is not simply that more information exists. The difference is that the information available has become increasingly granular and increasingly interconnected.

Modern analytical tools can identify relationships between variables that were difficult or impossible to measure only a few years ago. They can detect patterns, identify leading indicators, and evaluate organizational characteristics that may influence future claim outcomes.

Increasingly, underwriting is becoming less about reviewing static historical information and more about understanding the conditions that produce future losses.

This distinction matters.

Two organizations may have identical payrolls, operate within the same industry, and even possess similar experience modifications. Yet their future risk profiles may be materially different because their underlying operational characteristics differ significantly.

Granular data increasingly helps explain those differences.

Employee Wage Bands

Wage information has historically been viewed primarily as an exposure basis for premium calculation.

Increasingly, however, wage distributions provide meaningful insight into workforce composition.

PEOs frequently maintain employee-level payroll information that allows organizations to segment employees into wage bands and evaluate the percentage of employees within each compensation range.

For example, organizations may analyze:

Percentage of employees earning less than $40,000 annually

Percentage earning between $40,000 and $75,000

Percentage earning between $75,000 and $125,000

Percentage earning above $125,000

Viewed independently, wage information may appear relatively straightforward.

Viewed operationally, however, wage bands often reveal much more.

Compensation levels frequently correlate with experience, skills, workforce maturity, employee retention, and organizational stability. They may also reveal significant operational differences between organizations that otherwise appear similar from a traditional underwriting perspective.

Workforce Tenure and Retention

Employee tenure frequently serves as a proxy for organizational stability.

PEO census files often include hire dates, employment status information, and enrollment dates that allow organizations to evaluate workforce tenure characteristics.

Organizations can calculate:

Average employee tenure

Median employee tenure

Percentage of employees with less than one year of service

Percentage of employees with more than five years of service

These metrics matter because employees who remain with organizations longer generally possess greater institutional knowledge and operational familiarity.

Conversely, organizations experiencing elevated turnover frequently manage larger populations of newer employees who may be less familiar with processes, equipment, procedures, and workplace hazards.

The data does not necessarily establish causation, however, it increasingly helps identify conditions that may influence future claim outcomes.

Hiring Velocity

How quickly an organization is adding employees can also provide meaningful predictive insight.

PEOs routinely maintain monthly employee census information and payroll records that make workforce growth rates relatively easy to measure.

Organizations can evaluate:

Headcount growth rates

New hires as a percentage of total workforce

Payroll growth relative to employee growth

Seasonal hiring spikes

Rapid growth is not inherently problematic. Many high-performing organizations experience significant expansion.

However, accelerated hiring often introduces operational complexity. Training systems become stressed. Supervisors assume additional responsibilities. Larger percentages of employees become relatively new to their positions.

Underwriters increasingly recognize that the speed of organizational growth can influence future operational outcomes.

Employee Demographics and Age Distribution

Demographic characteristics also provide valuable context.

PEO census information frequently includes employee dates of birth and demographic information that allow organizations to evaluate workforce composition.

Organizations may calculate:

Average workforce age

Age-band distributions

Percentage of employees over age fifty-five

Age characteristics by classification code

Different demographic groups often exhibit different injury patterns, claim severities, recovery durations, and return-to-work outcomes.

As workforce demographics continue to evolve nationally, understanding these characteristics becomes increasingly important.

The objective is not to draw broad conclusions regarding any individual employee. Employment practices should always be performed according to the governing jurisdiction. The objective is to understand how aggregate workforce composition may influence organizational performance over time.

Geographic Concentration

Location matters in workers’ compensation.

PEOs routinely collect state payroll information and employee work location data that make geographic analysis increasingly accessible.

Organizations can evaluate a number of meaningful metrics.

Percentage of payroll by state

Percentage of employees by state

Payroll concentration ratios

Geographic diversification measures

These metrics are important because workers’ compensation systems vary considerably across jurisdictions.

Medical costs differ. Benefit structures differ. Litigation environments differ. Regulatory frameworks differ.

Two organizations with identical operations may experience substantially different outcomes simply because their workforces are concentrated in different jurisdictions. Understanding geographic concentration allows underwriters to better appreciate the operational environment in which risks actually exist.

Claims Development Patterns

Historical losses remain essential.

However, increasingly sophisticated analysis focuses not simply on ultimate outcomes but on how claims evolve over time, especially as claim patterns continue to evolve as societal behavior evolves.

Loss runs allow organizations to evaluate:

Paid versus incurred development

Reserve movement

Claim closure rates

Development by accident year

Frequency and severity trends

Claims development patterns often reveal emerging issues before those issues become fully reflected in traditional metrics.

An organization experiencing increasing reserve development may have operational issues that are not yet apparent through experience modifications.

Likewise, improving closure rates and favorable development trends may indicate operational improvements that historical summary statistics have not yet fully captured.

The direction of development frequently tells a story that static numbers alone cannot.

Return-to-Work Performance

Few operational processes influence workers’ compensation outcomes more directly than return-to-work execution.

PEO loss runs often provide information regarding:

Lost workdays

Temporary disability duration

Open claim duration

Medical-only versus indemnity claim percentages

Organizations can use these metrics to evaluate:

Average days away from work

Lost-time conversion ratios

Claim closure speed

Medical-only claim percentages

These measurements often reveal far more than claims management performance.

They frequently reveal organizational culture.

Organizations that successfully return injured employees to productive work often demonstrate strong communication, operational flexibility, and disciplined management processes.

In many cases, return-to-work performance represents one of the most controllable drivers of workers’ compensation severity.

Safety and Training Indicators

The presence of formal safety processes also provides meaningful predictive insight.

Submission materials frequently include:

Written safety manuals

New employee orientation procedures

Safety committee documentation

OSHA records

Safety certifications

Training schedules

While these indicators may appear qualitative, many can be measured quantitatively.

Organizations can develop scoring methodologies that evaluate:

Safety program maturity

Training frequency

Incident trends

Documentation completeness

The existence of documented safety processes does not guarantee favorable outcomes, however, organizations that consistently demonstrate operational discipline often exhibit more stable loss experience over time.

Increasingly, underwriters are attempting to measure these characteristics in a more structured and objective manner.

Industry-Specific Operational Characteristics

Class codes remain extraordinarily useful, however, they cannot explain every operational difference.

Two employers sharing the same classification code may operate in materially different ways.

Construction companies may differ according to:

Percentage of roofing operations

Project duration

Subcontractor utilization

Manufacturing operations may differ according to:

Degree of automation

Shift structures

Equipment intensity

Transportation companies may differ according to:

Fleet size

Driver tenure

Radius of operations

Healthcare organizations may differ according to:

Facility type

Patient handling exposures

Staffing models

Increasingly, underwriting seeks to understand how organizations actually operate rather than relying exclusively upon broad classification categories.

Operational details frequently explain future performance more effectively than historical labels alone.

The Future Is Increasingly Predictive

Workers’ compensation will always maintain a historical foundation.

Loss experience matters.

Experience modifications matter.

Classifications matter.

But the direction of the industry is becoming increasingly clear.

The workers’ compensation marketplace is steadily moving toward more individualized and increasingly predictive approaches to evaluating risk.

The objective is not simply to collect more information, but rather to collect better information that serves as a leading indicator of future performance.

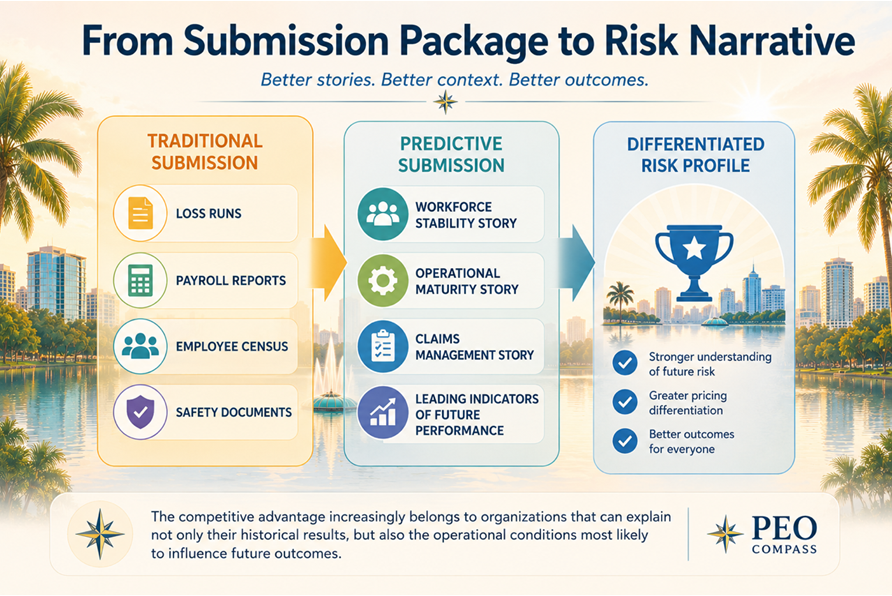

For PEOs, this evolution creates an opportunity.

Organizations that understand their data, measure operational characteristics thoughtfully, and demonstrate disciplined execution may increasingly distinguish themselves in underwriting conversations.

Ultimately, the most important question is

“What conditions exist today that are most likely to influence what happens next?”