Workers’ Compensation Insurance Rating Bureau (“WCIRB”) of California Votes to Authorize Double-Digit Rate Increase

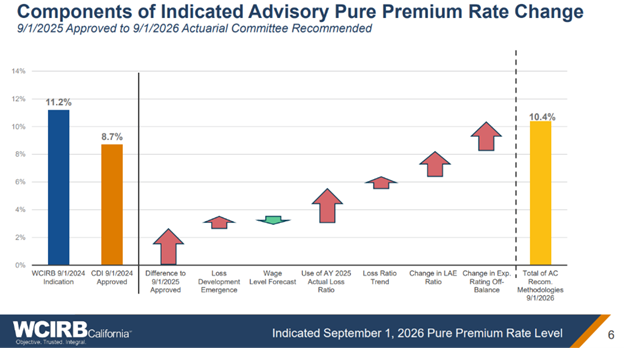

it was announced that for 9/1/26 the WCIRB is recommending workers’ compensation for pure-premium rates which will be on average for a 10.4% increase. Last year the WCIRB recommended 11.2% with the California Department of Insurance (“CDI”) settling in on 8.7% after discussion or 22% reduction versus what was proposed. It is more usual than not that the CDI will not merely accept the WCIRB recommendation, and while not always, they usually settle in below versus above the proposed recommendation.

The usual process mirrored in 2025 is for the WCIRB to recommend workers’ compensation pure premium advisory rates to the (“CDI”) sometime in the month of April with a 9/1 effective date for adoption. Note the adoption of the new rates is advisory and not mandated. After public hearings and discussion, the CDI and specifically the California Insurance Commissioner then render an ultimate order sometime in July for the 9/1 effective date. What components and factors are driving this upward trend in California rates?

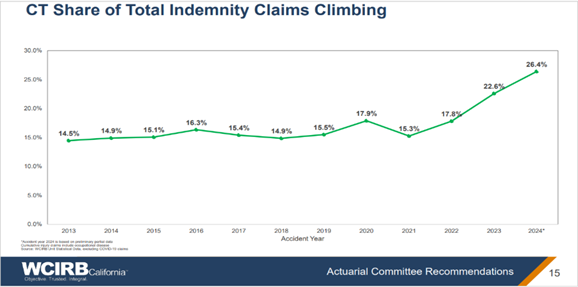

Trends and drivers that support the rate increase are an overall increase in loss ratio fueled by the continued surge in cumulative trauma (“CT”) claims (now 26% of all lost time claims State-wide and almost double that in certain regions like the LA Basin and Inland Empire), increase in Allocated Loss Adjustment Expenses (is this true cost containment or a place to fluff TPA and carrier margins in a soft market) and continued inflation in medical costs.

The proposed advisory pure premium rates are based on insurer losses and loss adjustment expenses incurred during accident years 2025 and prior trends can be seen in the charts below found from the WCIRB presentation to support the increase. Note that the full presentation can be found here:

The CT phenomenon can be seen below. As defined by the WCIRB “Some workers’ compensation injuries occur as a result of repetitive mentally or physically traumatic activities extending over a period of time. Although these cumulative trauma, or CT, claims can have exposure periods that span multiple years, by California law for workers’ compensation purposes, the liability for most CT claims is spread over the last year of injurious exposure. However, this last year of exposure will usually involve multiple insurance policies and often multiple insurers. CT claims are also more likely to involve multiple injured body parts, long delays between the injury occurrence and the time the claim was filed, representation of the claimant by an applicant’s attorney, and frictional costs such as liens and medical - legal costs.” A cottage industry amongst the legal community continues to push CT claims for WC claimants as they are very hard to prove one way or another, frequency is much higher post-termination and therefore potential misalignment with claimant, extend out longer periods of time with much higher percentage litigated and as a result, incur much higher average claim amounts

The aggregate result is after years of rate reductions in California and a spike in carrier profitability, the post-Covid years have not been so kind to workers’ compensation insurers. I have been waiting for the detailed WCIRB study as of 12/31/25 with current results in CA below as of 9/30/25. The market profitability as evaluated by combined ratio of the carriers is at the worst it has been since 2001 and spiked 12 points between ’23 and ‘2.

Reference: Quarterly Experience Report 2025 Q3.pdf

What are the top three things to do in light of this in California?

· The WCIRB has now advised for a combined 21.6% rate increase over the last two years with nothing on the horizon to help legislatively impact outcomes. Pricing will and is going up across the board and for those that set price using loss sensitive programs such as a Large Deductible, it makes the use of all actuarial, underwriting and risk management tools available essential in evaluating risk. Does that mean your book’s projected losses will go up this amount, no; they could go higher if not careful.

· Close any CT claim you can. These linger to no ones benefit and are the biggest driver of unexpected reserve increases which trigger collateral calls. Underwrite accounts that have a higher frequency of these claims, especially in Southern California where they are far more frequent.

· Watch the Allocated Loss Adjustment Expense (“ALAE”). The cost to contain cost is now upwards of $16k each lost time claim which is almost a 50% increase from 5 years ago. Understanding costs, when deployed and savings (?) associated with these fees should be set by the client and broker not the claims adjudication company (TPA or otherwise) that stands to gain from these charges (if possible and not carrier mandated).

Impact on the PEOs

Should the CDI adopt another meaningful increase for 9/1/26, PEOs should expect carriers to follow suit with higher renewal pricing, directly compressing PEO profit margins on California business. Beyond pricing, carriers operating in California face a binary choice: absorb the deterioration or act. Expect to see some combination of carrier exits from the state, tighter underwriting controls at renewal, and reduced appetite for PEOs with California-heavy books showing CT claim frequency.

For PEO leadership, the practical response is straightforward. Work with your agent now to identify and either remove or surcharge CT-heavy clients before renewal conversations begin. Reprice the California book with current loss trends in mind, not last year's rates. And ensure your TPA or internal carrier risk department is applying genuine scrutiny to California claims -not simply processing them.