NCCI Presumptive Benefits in Workers’ Compensation and COVID-19

Presumptive Benefits in Workers’ Compensation. Emerging Issues Before and After COVID-19.

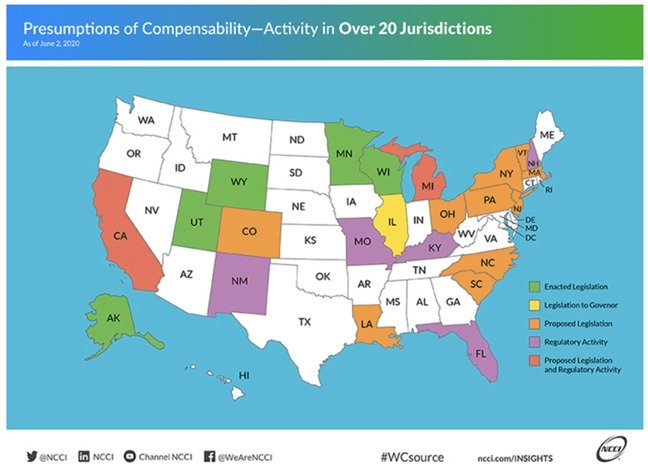

The National Council of Compensation Insurance ("NCCI") continues to further refine its cost estimates of COVID-19 for the 38 states that it oversees for the purposes of rate and rule making for workers' compensation. The most notable states not included in this study are California, New York and New Jersey which collectively make up about 40% of the workers' compensation premiums countrywide.The term "presumption of compensability" speaks to whether a COVID-19 case is deemed compensable solely by the nature of the afflicted's joe duties, scope and where work is performed. This is different in every state with new bills and laws being drafted and legislated every day.

The preemption legislation generally falls into three buckets:

- Bills that establish compensability presumptions for first responders (fire, police, ambulance) and/or certain healthcare workers (nursing homes, hospitals, home health etc)

- Bills that establish compensability presumptions for essential or frontline workers. This expands presumption into most all client-facing roles still necessary (grocery, pharmacist, mass transit, TSA, meat-packing, banking etc.)

- Bills that establish compensability presumptions for all employees in the state

Needless to say, understanding the expected costs to the workers' compensation system of any given state and the appropriate risk load to charge as a result starts with who will and will not "automatically" be covered and thus drive cost. As you will note below, there is a lot of activity in regard to this issue across the country.

You can access NCCI's state-by-state compensability tracker here.

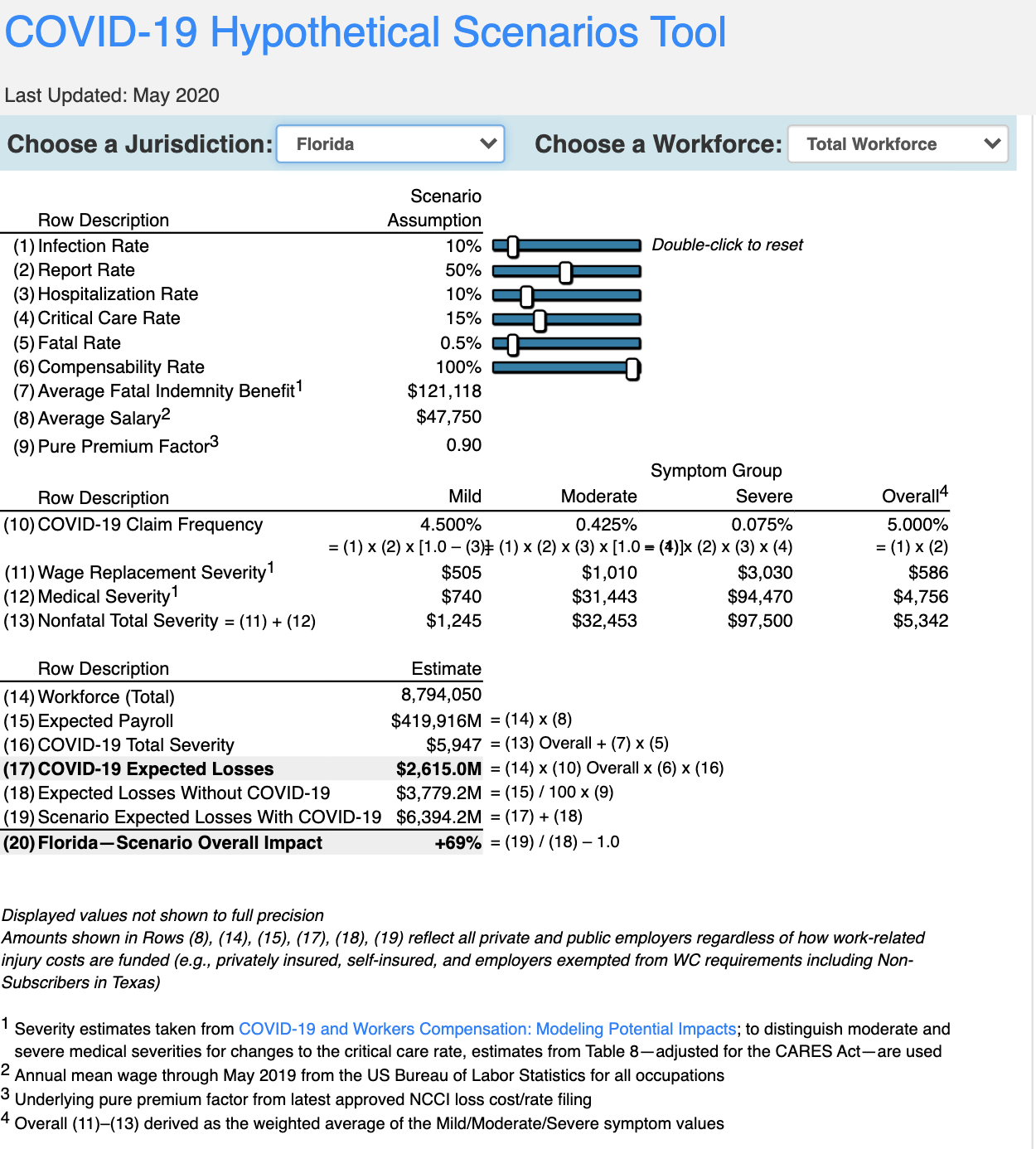

Additionally, the NCCI has built a free on-line COVID19 "Hypothetical Scenarios Tool" that really gets into the granular on expectation of costs by type of worker and symptom group as well as the expected risk load as a result thereof. Here is where the NCCI's middle of the road projection is as of their last study in April with the assumptions of all NCCI states and the total workforce presumed to have contracted COVID19 in an occupational setting. The scenario assumptions with slide bars below can be adjusted manually, but these are the "middle ion the road" defaults.

COVID-19 Hypothetical Scenarios Tools

Note in this scenario of the total workplace presumed to being exposed to COVID19 in all NCCI states, the expected additional risk load is +85%.Where I found this model to be even more interesting is on a state by state basis. Using same "total workforce" but now selecting just Florida. A 69% v 85% risk load and a fatality claim average being $121,118 v $341,111. Fatalities the most important risk and cost driver with "critical claims" coming in #2. Now if we do the same for Texas...

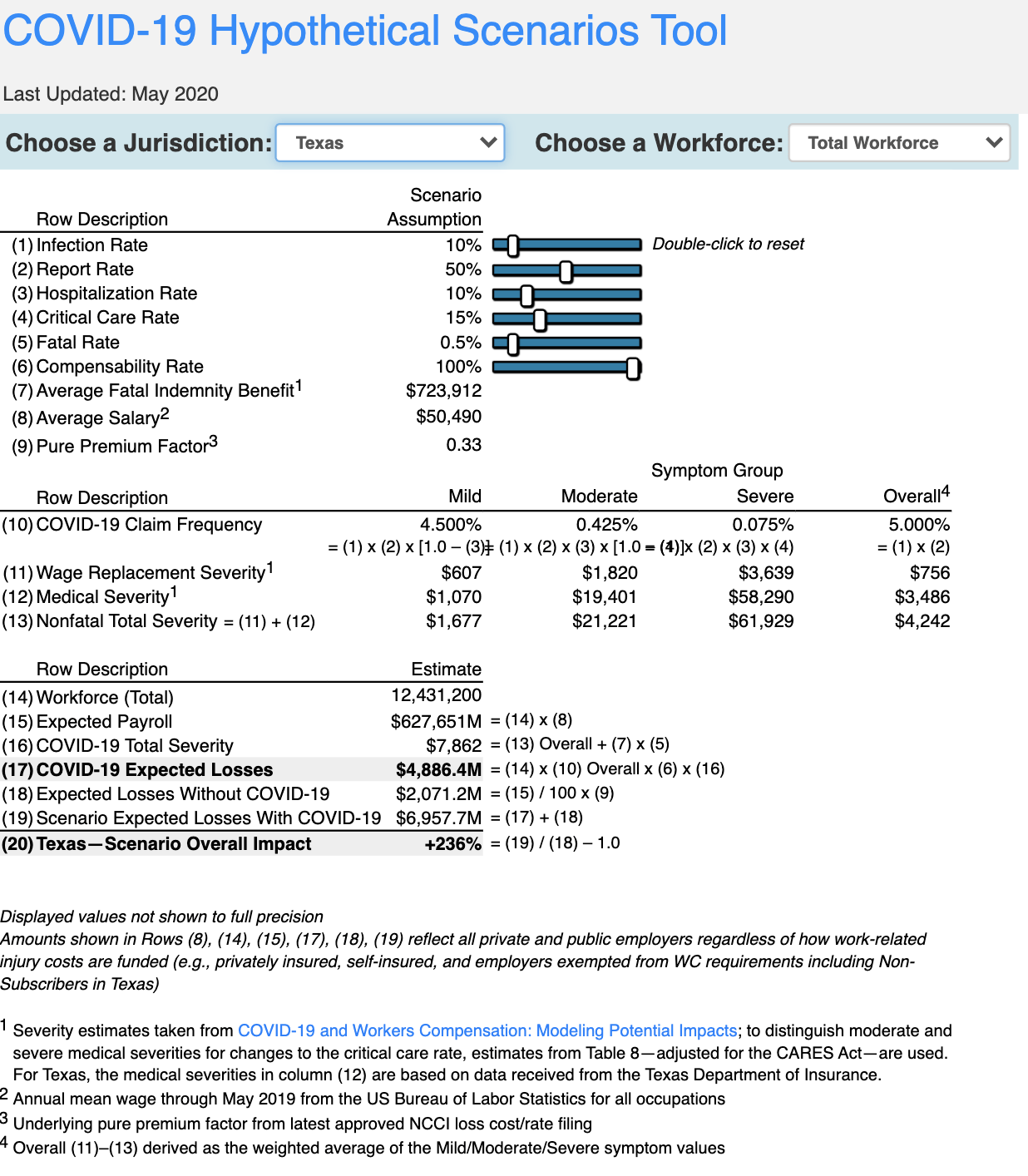

A 69% v 85% risk load and a fatality claim average being $121,118 v $341,111. Fatalities the most important risk and cost driver with "critical claims" coming in #2. Now if we do the same for Texas... The risk load almost triples the national average at 236% fueled by the cost of a fatality more than double the national average, or $723,912.This is a very powerful tool that shows all of the variables in play in the forecasting of expected costs in NCCI states due to COVID19. As this continues to be refined we will update you.Have a great weekend and stay safe.

The risk load almost triples the national average at 236% fueled by the cost of a fatality more than double the national average, or $723,912.This is a very powerful tool that shows all of the variables in play in the forecasting of expected costs in NCCI states due to COVID19. As this continues to be refined we will update you.Have a great weekend and stay safe.

Join the Conversation on Linkedin | About PEO Compass

The PEO Compass is a friendly convergence of professionals and friends in the PEO industry sharing insights, ideas and intelligence to make us all better.All writers specialize in Professional Employer Organization (PEO) business services such as Workers Compensation, Mergers & Acquisitions, Data Management, Employment Practices Liability (EPLI), Cyber Liability Insurance, Health Insurance, Occupational Accident Insurance, Business Insurance, Client Company, Casualty Insurance, Disability Insurance and more.To contact a PEO expert, please visit Libertate Insurance Services, LLC and RiskMD.